Grupo Pão de Açúcar (NYSE:CBD) - Time to clean the mess

After long overdue, GPA is finally optimizing their capital structure and should be able to capitalize non-core assets.

Near the top of the optimism with Emerging Markets, BRICS overhype two decades ago, French group Casino bought multiple controlling stakes in local LatAm Grocery Stores, Cash & Carry and Consumer Electronics chains, aiming to operate the synergies and ride the economic growth the region would experience. But, as we all know, the dynamism of the region dissuaded in 2014 until today, putting criticism about Casino’s wrong capital allocation and overleverage that almost dethroned the founder and chairman Jean-Charles Naouri, an ex-investment banker who made a fortune with LBOs, deep knowledge of corporate-law and operational turnarounds in french food retail chains like Rallye, Promodès and Monoprix.

One of the incursions of the group in Latin America was through Grupo Pão de Açúcar (GPA), the biggest Grocery & Consumer Electronics chain in Brazil led by Abilio Diniz. Operational efficiency and counter-cyclical bets turned GPA into a colossus local chain, intriguing the french to buy a minority stake in 1999. With Casino onboard, GPA was able to implement their strong culture in multiple acquisitions, turning around smaller chains into regional big players. But with the macroeconomic downturn, an increasing attriction between the french group and the brazilian’ management led Diniz to sell their controlling stake to the french group.

GPA under the French helm went through a complete societary mess: Via Varejo spin-off (BVMF:VIIA3), the creation of Nova Pontocom, which later merged with Cdiscount to create Cnova (EPA:CNV) and the controversial acquisition of Grupo Éxito (CB:EXITO), which is worth further exploration:

Éxito is a colombian cash-and-carry chain also controlled by Casino, which bought 54% of the shares in 2007 and remained the controlling shareholder whereupon payed disguised special dividends to themselfes by ‘simplifying the corporate structure in Latin America’: In 2015, Casino’s stake in GPA was sold to Éxito for a 59% premium, and later in 2019 Casino repurchased those shares at a discount to market capitalization and without distributing a single penny to minority shareholders - thanks to faulty corporate laws in both Colombia and Brazil. Casino’s next step to deleverage their core business turned GPA into their LatAm holding company. To do so, GPA announced a Tender Offer for Éxito and acquired 96.5% of the Colombian group, including Casino’s shares… Corporate Governance at its best (lmao).

After all this mess, GPA basically became uninvestable for most of LatAm fund managers due to its complicated governance and poor positioning amidst an economic dowturn… but there were two great assets within their holdings: Assaí and Éxito. I won’t delve further into Sendas Distribuidora, aka Assaí, (NYSE:ASAI), but basically its a cash-and-carry chain that GPA also bought in 2007 to ‘hedge’ against the trade down movement typical of economic downturns, i.e medium income households buying in cash-and-carrys instead in premium chains. In early 2021, GPA spun-off Assaí in a 1:1 ratio, which was well received from minority shareholders.

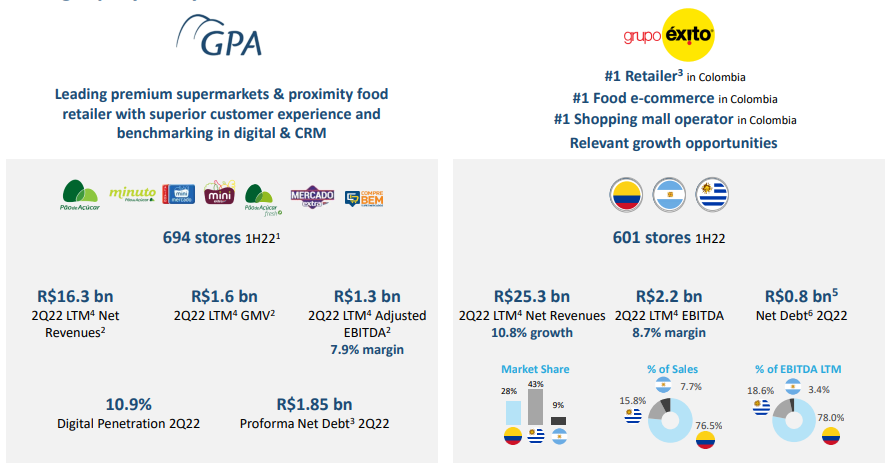

Today, GPA’s corporate structure includes:

GPA: Brazilian Chains Pão de Açúcar (premium food retail grocery chain), Extra (hypermarket food retail chain, a mix between a traditional cash-and-carry and grocery shops) and GPA Malls (Commercial Properties in Brazil);

Grupo Éxito: Colombian Chains Éxito (hypermarket chain, like Extra), Carulla (premium groceries) and SurtiMax / surtiMayorista (traditional cash-and-carry); Uruguayan Chains Risco and Géant; and Viva (Commercial Properties in Colombia):

So, where is the opportunity? GPA is going to spin-off their Éxito's stake to their shareholders.

Grupo Éxito is the #1 food retailer in Colombia and Uruguay, largest mall operator in Colombia and poised to benefit from i) explore significant growth opportunities bypassed due to GPA’s lack of investment resources; ii) stronger corporate governance, as Casino is expected to divest their stake, and iii) current valuation imply zero-to-none value for GPA’ Brazilian operations.

#1: Growth Opportunities

In the last GPA Investor Day, Éxito’s management shared a couple of interesting thoughts: due to their partnership with colombian super-app Rappi, the company has been able to strenghten their omnichannel experience, growing total orders to 58,6% yoy and 19% total platform sales in D2C; for bigger baskets, the group has its own apps to enable better experience. Other interesting point is that Éxito is repeating GPA’s Assaí success within their own smaller cash-and-carry business, called surtiMayorista, that Éxito expects to accelerate their expansion plans even further.

Other interesting point is their Real Estate footprint: Grupo Éxito’s company Viva is the largest shopping center operator in Colombia, with 34 assets and over than 758,000 sqm in GLA, occupancy rate of 96.3% and recurring EBITDA margin of 59.6%!

#2: Casino’s left behind

After the spin-off, Grupo Éxito is expected to have a 53% free-float and will still have Casino as a reference shareholder, but directly at this time. By taking Assaí’s spin-off as experience, we expect Casino to divest their stake in Éxito in 2H23 towards 2024 as Jean-Charles Naouri is in a rush for raising cash to pay off their holding co. debts. Therefore, without Casino, Éxito is expected to be a full corporation and can finally grow without any corporate governance troubles.

#3: Remaining GPA is negatively valued

Right now Éxito’s own market cap in Colombian Stock Exchange (CB:EXITO) is $950m, while GPA (NYSE:CBD) is worth $860m - despite GPA owning 97% of the company. EXITO low ADTV impacts relative valuations and is priced at discount of 4.5x to 5x EV/EBITDA, therefore RemainingCo is being priced for zero or even negative value within GPA’s current structure.

After the spin-off we deem reasonable to expect fair re-ratings for both Éxito (7x ~ 8x EV/EBITDA) and GPA Brazil + CNOVA (10x EV/EBITDA), therefore potentially making the case for a +100% upside from current prices (from ~$3/ADR to ~$6/ADR) in a 9 to 12 months timeframe.

Thanks for the article. Any insights on Grupo Mateus or Sendas Distribuidora.

I make it that Sendas could be at 3.5x on a P/FCF basis for FY25 with its stock hitting new lows. Obviously they have a lot of debt that they need to manage plus Brazil is a cheap market right now (https://live-pzena.pantheonsite.io/brazilian-equities-opportunities/) but wondered if you had knowledge of any particular company specific issues that are driving the stock price?

With Grupo Mateus, I don't know as much about the company. How are they managing to grow so fast? How do they compare to Sendas in terms of quality of the company? Are they the one to watch?

Thank you so much. This seems to be a very convincing idea, downside seems very limited and upside very serious. So my question would be... what's keeping others from looking at it? Why isn't anybody going crazy about this BN/BAM style? Any thoughts? Warm regards from Madrid :)